Can you afford to lose $175/month?

Did you know that the monthly payment on a $200,000 30 year mortgage would go up by a whopping $175 per month if mortgage rates go up slightly from 3.5% to 5.0% like they were just 3 short years ago?!

Here are four reasons why mortgage rates could go back up, costing you at least $175/month:

#1 – End of the Fed’s $2 Trillion “Quantitative Easing” Programs

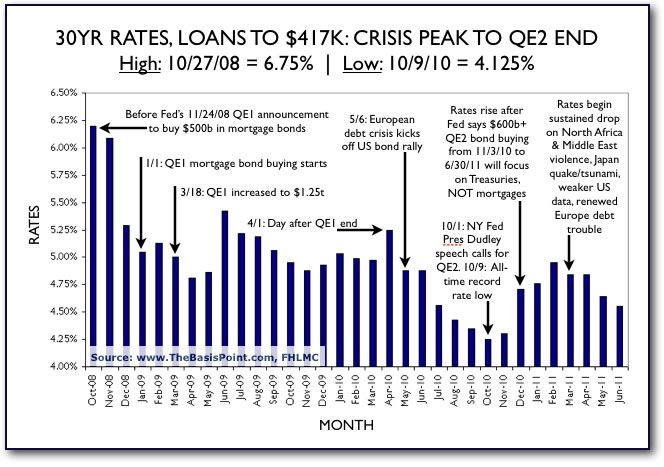

Here’s a chart showing how $2 trillion of government intervention drove 30 year mortgage rates down by over 2% in the last few years:

The Fed’s unprecedented intervention in the bond market was known as “Quantitative Easing” because the Fed increased the “quantity” of the US money supply by purchasing over $2 Trillion of mortgage bonds and US Treasuries. This enormous government intervention in the markets (known as QE1 and QE2) has consistently kept mortgage rates down below 5% during the last few years.

As unemployment lessens and the economy recovers, the Fed will stop their intervention. In fact, they have indicated that in the future, they may even decide to SELL some of the $2 trillion in bonds that they have purchased over the past few years. This leaves us wondering, “What happens when the bond market loses its biggest buyer?” Further, “What happens when the biggest buyer becomes the biggest seller?” This undoubtedly means that interest rates are more likely to be higher than lower in this scenario.

#2 – Uncertainty Surrounding Fannie, Freddie, and the FHA

From 1996-2003, the government was steadily involved in 85-90% of mortgages. From 2003-2008 we saw the rise of the sub-prime mortgage and the government’s involvement dropped to about 60% of mortgages. After the mortgage crisis, the government’s involvement has risen to almost 100% of all mortgage transactions. If you track interest rates over these same periods you can see the largest spread between interest rates (government vs non-government) was during the period with the least amount of government involvement.

The government’s involvement in the mortgage markets is part of the reason why mortgage rates are so low today. In fact, mortgages that don’t include any government involvement (like jumbo mortgages) carry interest rates that are 0.25% – 2% higher than mortgages that do include government involvement (like conforming and FHA mortgages). There are many proposals on the table now to reduce the role of Fannie Mae, Freddie Mac, and the FHA in the US mortgage markets so there is the potential to see rates go higher by .25% to 2% depending on what the final outcome of the government’s involvement in the mortgage process is determined to be.

#3 – Over-Regulation of the Mortgage Market

The Dodd-Frank financial reform law and other regulations have resulted in tougher lending standards and higher legal costs for the mortgage industry. As you can expect, many mortgage lenders will be passing these higher costs along to the borrowers who borrow money from them.

For example, one of the new rules mandates that all mortgages that aren’t considered “qualified” will carry higher interest rates. There is a lot of debate going on right now about the definition of “qualified”, but generally you can expect that most adjustable rate mortgages, interest-only mortgages, and loans that involve less than a 20% down payment will carry higher interest rates in the future than they do today.

#4 – Skyrocketing US Government Debt

There are two ways that the ballooning US government debt situation will drive mortgage rates higher:

1 – More Supply than Demand

More government debt = more supply of bonds in the market

More supply of bonds = lower bond prices

Lower bond prices = higher interest rates

2 – Risk of More Inflation

More government debt = higher risk of inflation

Higher risk of inflation = higher mortgage rates

The main question is not whether interest rates are likely to go up in the future… that answer is obvious. The main question is what can you do about it RIGHT NOW?

What should do with your current mortgage?

What are your options when it comes to buying a new house and locking in a low interest rate?

How can you take advantage of the clearance sale going on in the mortgage and housing market without risking your family’s financial future?

My clients face tough questions like these every day. That’s why we are here to help people like you make the right decisions. If you need advice, or know someone who does, please contact us so that we can help you.